1.Introduction

The raison d’être of healthcare organizations lies in contributing to the protection of health, which consists of improving the effects of their activities on the health conditions of individual patients and the community. Healthcare organizations use human, material, and financial resources to accomplish this mission.[1] Thus, the value created can be measured by the patient outcomes achieved per dollar expended.[2] Service cost is a core issue for healthcare managers and providers of funds, whether public or private.[3] Costing practices contribute to the definition of healthcare organizations’ strategies and are used to design Diagnosis Related Group (DRG)-based funding systems.[4] Inefficiencies preclude using resources for alternative purposes and fuel financial crises with consequent governmental resource cutbacks.[5, 6] Managers, physicians, and other healthcare staff are requested to deliver high-quality services at the lowest possible cost.[7] Being aware of the expenses of services may enable them to allocate resources more efficiently and avoid waste.[5, 8] Then, the cost analysis must be accurate and provide managers and physicians with reliable information[9] to stimulate the efficient use of resources and avoid side effects on service continuity.[3, 7, 8]

A growing body of literature exists on healthcare service costing and its importance as a driver for therapeutic choices.[6, 9,10,11] However, DRG costing, cost awareness, and the importance attributed to the economic factors have seldom been considered in the same study, and there is a lack of studies extending this kind of analysis to different classes of hospital staff. This paper intersects the importance attributed to the Economic Factors (economic factors importance [EFI]) with Economic Factors Awareness (EFA) among hospital staff, thus detecting informative gaps for physicians, nurses, and administrative employees. To do this, we first performed micro-costing for DRG 546 and then submitted a survey on EFA and EFI to the staff of an Italian children’s hospital. EFA refers to DRG rates as well as DRG costs. Moreover, awareness implies that staff members: (a) consider themselves capable of estimating economic aspects and (b) their evaluations are correct. Thus, awareness is not considered a dichotomous variable in this context; instead, it is treated as a discrete qualitative variable, with responses assigned values based on their adequacy.

The DRG system is a classification system for patients discharged from a hospital based on the principle that similar diseases treated in similar hospital departments with similar procedures result in approximately the same resource consumption. The assignment of each hospitalization to a specific DRG is carried out through software that gathers patient information from the Hospital Discharge Form. Diagnoses and diagnostic and therapeutic procedures are described in the Discharge Form using the ICD-9-CM classification system. In Italy, the latest ICD version defined by the World Health Organization has not yet been adopted. Currently, the Italian National Health System in Italy has defined 579 DRGs. With the decree of 18 October 2012, the Ministry of Health associated each DRG with a reimbursement rate based on the estimated average cost of the hospitalization. Therefore, the DRG system is used as a remuneration mechanism, ensuring that hospital funding depends on the volume and complexity of healthcare provided but is independent of the length of stay (LOS) and actual costs incurred: this funding system is aimed at improving the efficiency of healthcare organizations by making them accountable for the use of resources. Law 133/2008 requires hospitals to audit at least 10% of medical records to verify their appropriateness and correspondence with the Discharge Form. This audit aims to limit upcoding, i.e., the attribution of unnecessary or not actually provided medical services.

Concerning cost analysis, three factors influence its quality:[1] relevance, standardization, and accuracy. The more specific the cost object, the more relevant the cost information: detailed cost data may modify physicians’ approach to using resources to treat patients.[12, 13] Standardizing costing methodologies is necessary to allow comparisons among hospitals. Differences among cost estimations are not problematic when they reflect actual variations in the service composition or the patients’ case mix;[14] however, lack of standardization becomes critical when it corresponds to different costing approaches applied for the same treatment[15] and, even more, when costs of healthcare services are used to define the rates in the context of a DRG-based funding system.[16] Accuracy refers to the congruence between the costing methodology adopted and the evaluation purpose. For example, fixed overheads should remain unallocated when irrelevant to a specific managerial decision.

Costing methodologies for healthcare services can be categorized into four wide-ranging classes:[17, 18] micro vs. gross costing, top-down vs. bottom-up costing. Micro and gross costing methodologies are identified considering the accuracy of resource identification. Micro-costing creates a detailed list of resources used for a patient’s care. Every facet of a patient’s hospitalization,[19] from admission to discharge,[20] is estimated from direct observation. Its application is justified when cost estimates of a specific treatment are still unknown or when the purpose is to analyze cost variations between two or more healthcare techniques.[16, 20, 21] Gross costing defines cost components at a highly aggregated level (e.g., inpatient day).[4]

The second classification of healthcare costing methodologies considers whether the cost allocation approach proceeds top-down or bottom-up. Top-down costing values cost components by separating out costs from comprehensive sources (e.g., annual accounts). Indirect costs are allocated to responsibility centers and then apportioned to the cost objects according to appropriate allocation bases.[17, 22] Most of the organization’s costs are indirect; direct costs (i.e., costs incurred due to a specific cost object) are much less frequent.[5] Bottom-up costing methods estimate costs by identifying resources directly used for a patient, resulting in patient-specific unit costs. While top-down approaches usually emphasize average costs, bottom-up techniques are adopted to measure cost variations among different medical centers or patients.[23, 24] With bottom-up costing, resources are identified by questionnaire, direct observation, or the patient’s clinical records. It is considered more accurate than top-down costing; however, it can be used only for individual patient follow-ups.[10, 24]

Overheads can be allocated to services or patients through traditional volume-based or activity-based costing (ABC) techniques. In traditional cost accounting systems, indirect costs are allocated to the responsibility centers in a cascading (step-down) process; from the responsibility centers, costs are then allocated to the healthcare services or patients. Traditional volume-based costing uses parameters such as labor, machine hours, and square meters.[1, 25, 26] Its main advantage is the relative simplicity of system development. ABC systems, on the other hand, consider the activities that must be performed to deliver a service and the resources that these activities absorb, regardless of which center of responsibility they are performed in; thus, this system allocates resources taking in consideration the complexity of healthcare services, which depends on the activities to be performed. Healthcare is a highly customized job:[8] costing each activity and considering all activities absorbed by a specific service or client allows more precise cost allocations.[27] ABC considers a patient’s pathway as a sequence of resource-absorbing activities. Although scholars recognize the benefits of ABC,[28] its adoption rate is relatively low due to several difficulties in implementing it.[1]

There is quite an extensive literature on cost awareness in healthcare: in general, an information gap is reported. Guidet and Beale state that intensive care unit (ICU) directors would like to have access to a detailed description of income and spending and are willing to integrate cost constraints into daily practice when the system makes it practicable.[6] Chandawarkar et al.[5] found a gap in assessing the cost of postoperative complications by 53 residents in the general surgery program medical staff. They introduced an educational tool that measurably improved the overall understanding of the cost of care. In a study conducted in the UK, a questionnaire sent to 139 experts revealed that 97.1%, 95.7% and 97.1% overestimated the cost of a 14Ch urethral catheter, Ciprofloxacin and Sildenafil, respectively, while 78.4% and 84.9% of responders underestimated the cost of a JJ ureteric stent and Solifenacin, respectively.[29] Schilling[30] assumed that private medical professionals who provide services and bill for them know the cost of most medical tests. In public health systems, on the other hand, physicians may be aware of costs because of their experience in the field, as well as personal responsibility for meeting the financial constraints imposed by the organizations’ budgets. The author administered an anonymous questionnaire to thirty physicians about the costs for several items used to diagnose pulmonary embolism: the study demonstrates a lack of EFA and no significant variation in the accuracy of estimates among age groups. Other studies come to different conclusions concerning the effect of years of experience on cost awareness. Hernu et al.[31] found that French anesthesiologists’ cost awareness deficit was particularly evident among young physicians, thus suggesting a relation between years of professional experience and cost awareness. This study involved junior and senior physicians in 99 French intensive care units who were asked to estimate the true hospital costs of 46 selected prescriptions commonly used in critical care practice.

Levine D. et al.[8] showed that EFA led to significant cost containment in the Hospital for Special Surgery (New York, NY) through the recycling of wasted implants, reduction of costly implants, and reduction of unnecessary supplies. The cost reduction program did not sacrifice the quality of medical care and contributed to a breakdown of barriers between medical staff, administration, and finance. Ryan, Rogers, and Robb[14] assessed cost awareness among 326 surgeons in different Hospitals in Ireland: the study proved that only 5.7% of surgeons received training in health economics and needed more knowledge of the cost of surgical equipment. Mulholland et al.[18] conducted a study that involved 49 radiology trainees: they found that the cost of devices was overestimated 32.3% and underestimated 48.9% of the time. Fabes et al.[32] administered a survey asking to report the cost of different types of scans, visits, medications, and tests. The study targeted four clinical cohorts: medical students, Senior House Officers/Interns, Mid-grade Senior registrars/ Residents, and Consultant/Attending Physicians in six hospitals in the United Kingdom, the United States, Australia, New Zealand, and Spain. The analysis focused on the differential between the perceived/recalled cost and the actual cost. Only 13% of the estimations provided by the 705 clinicians were within 25% of the actual cost.

Our study combines DRG costing, EFA, and EFI to detect informative gaps among different groups of hospital staff, which are classified by role (physicians, nurses, administrative staff) and years of seniority. The administrative staff deal with economic data daily, so expecting them to have a fair knowledge of the DRG rates and costs is reasonable. The medical staff is less involved in economic matters. Still, physicians are engaged in economic aspects since they must make decisions in the patient’s treatment pathway. Therefore, one can expect some awareness of physicians on economic aspects, although less than for the administrative staff. Since nurses have less decision-making responsibility than the medical staff, they may be less aware of economic factors. Thus, it can be assumed that:

H1: Among the three classes of hospital staff (i.e., physicians, nurses, and administrative), nurses present the lowest EFA.

H2: Administrative staff and physicians place greater importance on EFI compared to nurses.

Within the different classes, the level of EFA (i.e., economic factors awareness: DRG rate and costs in different clinical care activities) may also depend on the years of seniority: it is reasonable to assume that longer work experience brings a more intensive involvement in the economic aspects.

H3: Staff with extended work experience develop greater EFA.

After estimating the EFA of different categories, it is possible to intersect this information with EFI (economic factors importance) attributed by different staff classes.

2.Methods

This study considers DRG 546 (i.e., Vertebral arthrodesis except cervical with spinal deviation or malignant neoplasm) treatments performed at IRCCS (i.e., Institute for Hospitalization, Care, and Research) “Burlo Garofolo,” a renowned pediatric and maternity care specialist center in Italy. This hospital is a public organization. In Italy, the National Health System is 80% financed through general taxation. The rest comes from patients’ contributions (out-of-pocket or insurance coverage). These funding sources must cover the costs of healthcare services that the law considers essential for all resident citizens. Financial resources gathered from general taxation at the national level are allocated to the Regions considering the resident population; then, the Regions allocate the resources to the healthcare organizations.

In 2019, the “Burlo Garofolo” hospital’s operating revenues amounted to EUR 76 million (95 million in 2023), including four main sources of funding: 43% of income came from charges for healthcare services provided (i.e., DRG rates), 37% from the allocation of the regional health fund, 11% from research grants and 3% from the patients.

Considering the volume of overall cases in the hospital and the relative volume of cases treated in the individual pediatric clinical areas, Burlo Hospital has modest experience but a high focus.[16] DRG 546 is the 49th by frequency in the institution. However, considering the ministerial weight given to the DRG (i.e., care complexity) and the frequency of surgery, this DRG is the third for the economic impact on the hospital.

The analysis used accounting data for 2019; these data were considered more reliable considering the impact of the COVID-19 pandemic crisis on hospital activities in 2020 and 2021. The study was developed in two phases: DRG cost estimation and EFA/EFI survey.

The hospital had detailed accounting data on the cost of all resources but lacked a cost accounting system to estimate each DRG. Thus, the study’s first phase served as a test for introducing a costing system. The retrospective cost estimation was performed on all patients (55 cases) coded with DRG 546. Not all patients presented the same degree of complexity. Only 16 patients had Adolescent Idiopathic Scoliosis without any other associated secondary diagnosis. Forty-five patients also associated scoliosis with kyphosis, which increases the complexity of surgical treatment due to a higher risk of complications. Other secondary diagnoses have been associated with the primary one, including infantile cerebral palsy (8 cases), hemivertebra (4 cases), paraplegia (3 cases), ataxia (1 case), Prader-Willi syndrome (1 case), spinal muscular atrophy (1 case). Less complex patients within the same DRG are more lucrative: this leads to the phenomenon of patient selection (vertical cream skimming), which, however, has been reduced over time as the number of DRGs has increased. The hospital considered in this study treats extremely complex cases and is a national center for the surgical treatment of scoliosis of various etiologies in the pediatric age. A specialization towards DRG 546 (horizontal cream skimming) can be recognized.

The total number of hospitalization days for patients classified in DRG 546 was 963, corresponding to an average LOS of 17.5 days. The standard deviation was quite high (16 days) since the average was influenced by 6 patients whose LOS exceeded 36 days due to complications, up to a maximum of 82 days. Excluding these patients, the average LOS would have been 12.6 days. The minimum LOS of a DRG 546 patient was 6 days. The DRG rate defined by the Ministry of Health assumes of 25 hospitalization days: apart from the aforementioned six patients, the LOS of all other patients was lower than 25 days.

The hospital department “Management Control” provided cost and activity data and organizational information from the operating facilities involved in the patient’s diagnosis, care, and treatment pathway.

A top-down micro-costing methodology was chosen, with indirect costs allocated through ABC to achieve greater accuracy. The cost analysis observed the following steps: analysis of the pathology, reconstruction of the patient’s pathway, organizational analysis of the personnel belonging to the structures involved, analysis of instrumental and diagnostic investigations, identification of cost drivers to highlight causality between the service provided, the activities performed, and the resources used.

Direct observation and structured interviews with the medical and nursing staff mapped the patient pathway. Moreover, the information contained in each Hospital Discharge Form and the Operative Registry regarding patients with DRG 546 was used. The documents showed the number of days spent in the surgical department and the ICU, the prostheses implanted during surgery in the operating room, and all the patient’s diagnostic and therapeutic interventions.

Expenses incurred in support functions (e.g., administration, facility maintenance, and cleaning) were not considered because the analysis aimed to assess the service’s production cost and to examine the cost awareness of the physicians and other clinical staff.

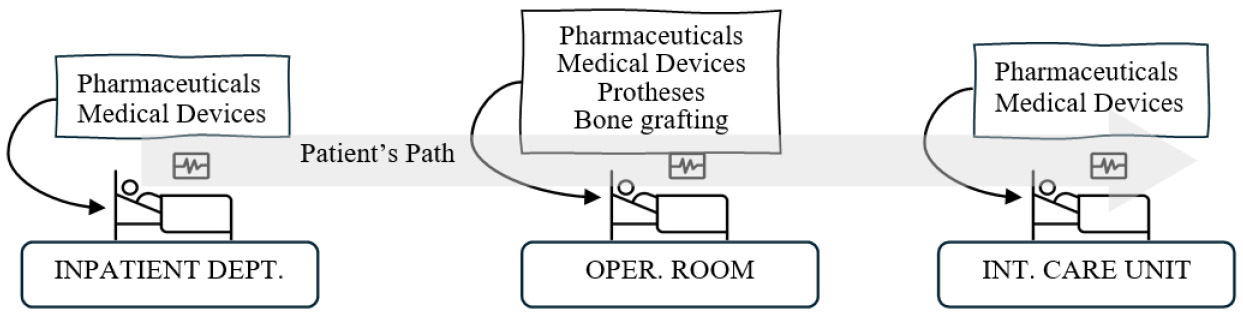

The costs of implantable prostheses, bone grafts, medical devices, and drugs used during hospitalization, ICU, and Operating Room activities were directly attributed to the patients (see Figure 1). The data extracted from each Hospital Discharge Form and Clinical Record allowed for timely imputation of the cost to the individual patient. A “Minimum Standard Set” of medical devices and drugs was evaluated by mapping a standardized pathway.

Figure 1.

Costs directly attributed to the patient

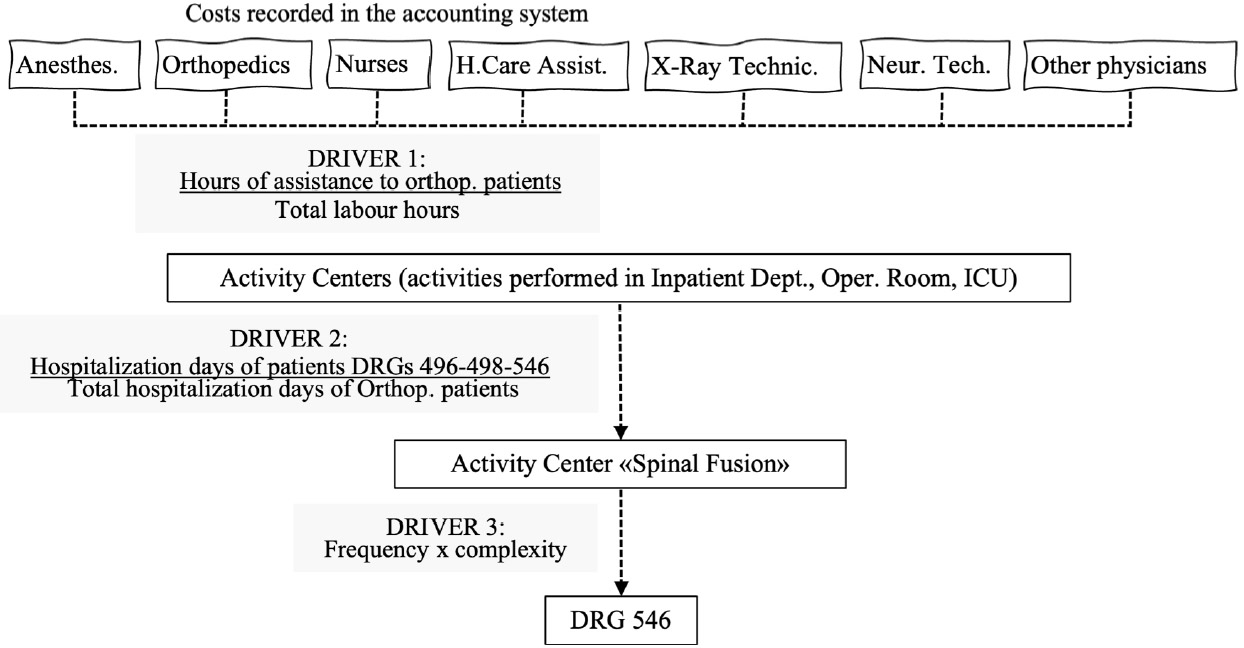

Top-down micro-costing associated with Activity-Based Costing allowed the allocation of indirect costs, i.e., personnel involved in patient care, diagnosis, treatment, and electromedical equipment. Following Cooper & Kaplan,[27] the cost of centers identified in the financial accounting system (e.g., the salary of nursing staff in the surgical center) was reallocated to “activity centers” (e.g., for the nursing staff of the surgical center: scheduled surgical activity in the operating room) using labor hours for each activity performed as a driver. The costs of activities was then allocated to the activity center “Spinal Fusion,” which provides DRGs 546 (Vertebral arthrodesis except cervical with spinal deviation or malignant neoplasm), 496 (Vertebral arthrodesis with combined posterior and anterior approach), and 498 (Vertebral arthrodesis except cervical without complications). Costs were allocated to this activity center considering the total LOS of patients classified in DRGs 496/498/546 compared to the total LOS of all orthopedic patients. Finally, the cost of DRG 546 was separated from that of the other DRGs supplied by the “Spinal Fusion” activity center considering the frequency of the provision of each DRG, weighted by their complexity measured through the parameters provided by Ministerial Decree 12/18/2008 about the average resource consumption of each hospitalization. The higher the Ministry parameter, the higher the care burden; consequently, it was considered a proxy indicator of inpatient complexity based on the assumption of a positive correlation between clinical complexity and resource consumption. This cost-allocation process can be visualized in Figure 2.

Figure 2.

Top-down microcosting

After completing the cost estimation phase, a survey was submitted to analyze the staff’s EFA and EFI. All subjects in the study participated in the care and organizational management of the patient undergoing DRG 546. The questionnaire was administered to managerial and non-managerial healthcare and administrative staff of the following departments: Financial Management, Planning and Control, Orthopedics and Traumatology, Management of Health Professions, Surgery, Anesthesia and Reanimation, and Pediatric Surgery Inpatient area. Medical directors, nurses with coordination responsibility, nurse executives, administrative assistants, and administrative managers were involved. The questionnaire asked healthcare and administrative professionals to indicate which value, among 5 possible answers, was the most plausible for the DRG 546 rate or cost of a specific resource. The research board of the hospital approved the questionnaire’s submission at the end of September 2022. It was administered anonymously through an internal digital platform of the Institute (RedCap) at the beginning of October 2022. Sixty-one questionnaires were correctly completed and submitted, corresponding to a return rate of 73%: 22 doctors, 36 nurses, and three administrative employees.

Respondents who believed they could estimate the DRG rate and costs were also asked to choose, among five alternatives, the correct value of the rate and costs. The correct answer was scored 1; for the other four possible answers, an increasing decrement of 0.25 was charged the more incorrect the answer was. Therefore, the score for each question ranged from 0 to 1. The answer “I could not provide an estimate” was also given a score of 0. The maximum achievable total score was then normalized on a scale from 0 to 10, and the average value (i.e., 5) was defined as the threshold. The data collected about the awareness of the DRG’s economic aspects then intersected with the importance of economic factors such as the DRG rate and the cost of resources in different phases.

To assess the average importance attributed to economic factors by the different professional groups, a weighted average was calculated by assigning numerical values to each of the three possible responses: very important = 1, important = 0.5, and unimportant = 0.

The hospital staff was categorized as follows by role and years of seniority:

(a) Role: medical staff (physicians, directors of departments), nursing staff (nurses, healthcare assistants, technicians), administrative staff.

(b) Years of seniority in their professional role: 0-5, 6-15, 16-20, > 20.

3.Results

As shown in Table 1, the margin for the hospital from DRG 546 to cover overheads is quite low. In Table 1, costs refer to a specific patient: staff costs are based on the daily cost reported in Table 2, times the number of days the patient spends in the different departments. The LOS for the patient considered in the table was 20 days: 17 days in the Inpatient Department and three days in the Intensive Care Unit. Direct costs were detected from the surgical register (i.e., a document written by the doctors after completing surgery).

| Inpat.Dept. | 634 | 4,763 | 2,137 | 28 | 7,562 | ||||||

| Operat. Room | 957 | 1,041 | 1,613 | 17 | 57 | 1,350 | 1,522 | 5,538 | 768 | 12,863 | |

| Inten. Care Un. | 930 | 1,473 | 161 | 37 | 2,601 | ||||||

| Others | 212 | 212 | |||||||||

| Cost (C) | 1,591 | 1,971 | 7,849 | 2,315 | 85 | 1,350 | 212 | 1,559 | 5,538 | 768 | 23,238 |

| DRG rate (T) | 24,822 | ||||||||||

| Margin (T-C) | 1,584 | ||||||||||

| Inpat. Dept. | 37 | 280 | 126 | 28 | ||||||

| Operat. Room | 957 | 1,041 | 1,613 | 17 | 28 | 1,349 | DC | DC | DC | |

| Inten. Care Un. | 310 | 491 | 53 | DC | ||||||

| Others | 60 | |||||||||

Regarding EFA, Table 3 classifies respondents by professional group, and 13 economic factors are considered. Most of the responding doctors and nurses considered themselves unable (Un.) to estimate the DRG’s economic aspects. Moreover, the table shows that most of those feeling confident made a wrong estimate (Wr.An.). Data were also collected considering the employees’ years of experience, but they are not reported here due to their scarce significance. Given the limited size of the sample examined, the

| DRG rate | Administr | 1 | 2 | 0 | .000 | Nursing Intensive Care | Administr | 0 | 1 | 2 | .27 |

| Nursing | 32 | 2 | 2 | Nursing | 19 | 7 | 10 | ||||

| Medical | 11 | 2 | 9 | Medical | 13 | 5 | 4 | ||||

| Medical act. | Administr | 0 | 0 | 3 | .01 | Neurophys. Technician | Administr | 1 | 2 | 0 | .02 |

| Othopedic. | Nursing | 29 | 1 | 6 | Nursing | 29 | 4 | 3 | |||

| Inpat. Dept. | Medical | 15 | 3 | 4 | Medical | 12 | 3 | 7 | |||

| Medical act. | Administr | 0 | 1 | 2 | .001 | Health Care Assistant Inpat. Dept. | Administr | 1 | 1 | 1 | .17 |

| Surgical. | Nursing | 29 | 2 | 5 | Nursing | 26 | 2 | 8 | |||

| Intervent. | Medical | 9 | 6 | 7 | Medical | 18 | 0 | 4 | |||

| Medical act. | Administr | 0 | 1 | 2 | .003 | Health Care Assistant Int. Care. | Administr | 1 | 0 | 2 | .32 |

| Anesthesiol. | Nursing | 22 | 3 | 11 | Nursing | 25 | 2 | 9 | |||

| Inten. Care. | Medical | 4 | 4 | 14 | Medical | 18 | 1 | 3 | |||

| Medical. Act. | Administr | 0 | 0 | 3 | .000 | Health Care Assistant Surgic. Inter. | Administr | 1 | 0 | 2 | .12 |

| Anesthesiol. | Nursing | 25 | 4 | 7 | Nursing | 24 | 5 | 7 | |||

| Surgic. Inter. | Medical | 4 | 4 | 14 | Medical | 18 | 3 | 1 | |||

| Nursing | Administr | 0 | 3 | 0 | .01 | Medical Devices | Administr | / | 0 | 3 | 1.0 |

| Inpatient Dept. | Nursing | 22 | 6 | 8 | Nursing | / | 6 | 30 | |||

| Medical | 15 | 1 | 6 | Medical | / | 4 | 18 | ||||

| Nursing | Administr | 0 | 1 | 2 | .23 | ||||||

| Surgical | Nursing | 22 | 4 | 10 | |||||||

| Intervent. | Medical | 14 | 2 | 6 |

As shown in Table 4, the group of nurses attached less importance to EFI than the doctors and administrative staff.

| Physicians (22) | 1 | 11 | 10 | 22 | 0.70 |

| Nurses (36) | 5 | 19 | 12 | 36 | 0.60 |

| Administrative staff (3) | 0 | 1 | 2 | 3 | 0.83 |

The results of the questionnaire on EFA and EFI are summarized per hospital staff class in Table 5. The results can be visualized in more detail through a graph.

| PHYSICIANS (22 respondents) | ≥ 5 ( |

< 5 ( |

| Very important | 2 (33.3) | 8 (50.0) |

| Quite important | 4 (66.7) | 7 (43.8) |

| Not important | 0 (0.0) | 1 (6.2) |

| NURSES (36 respondents) | ≥ 5 ( |

< 5 ( |

| Very important | 4 (50.0) | 8 (28.6) |

| Quite important | 4 (50.0) | 15 (53.6) |

| Not important | 0 (0.0) | 5 (17.9) |

| ADMINISTRATIVE STAFF (3 respondents) | ≥ 5 ( |

< 5 ( |

| Very important | 2 (66.7) | 0 (0.0) |

| Quite important | 1 (33.3) | 0 (0.0) |

| Not important | 0 (0.0) | 0 (0.0) |

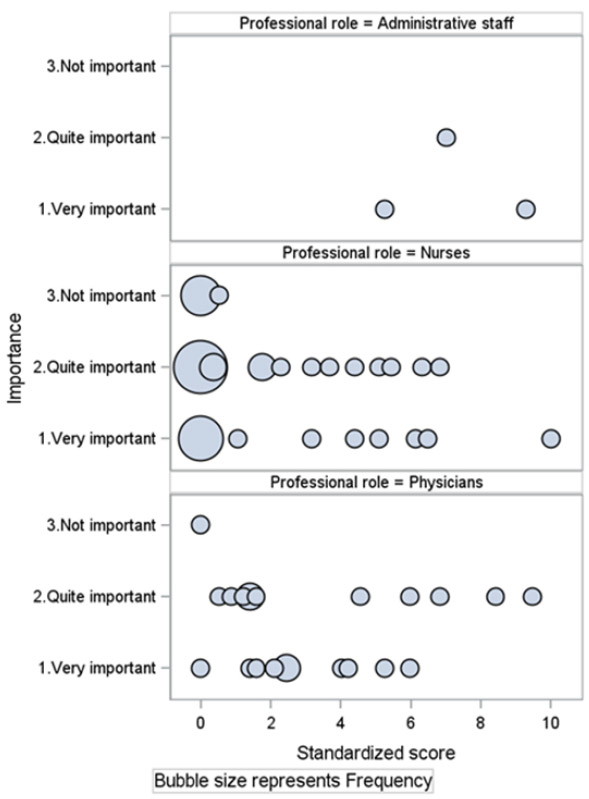

Figure 3 illustrates the intersection between EFA and EFI for each professional group. The size and position of the bubbles represent the number of respondents and the score they obtained, respectively.

Figure 3.

Importance attributed to EFI and staff’s EFA standardized score: Overall view

4.Discussion

4.1The information gap

Unsurprisingly, the administrative staff and physicians felt more confident about economic aspects than the clinical staff. Overall, in nearly 90% of cases, administrative employees believed they could provide an evaluation; moreover, all scored more than 5, and one approached a score of 10. The average normalized score for the administrative staff was 7.19/10. Physicians declared they could not provide the requested estimate for 57% of the analyzed aspects; the percentage was even higher for nurses (70%). Only 10% of the nurses’ answers were right (13% for physicians), suggesting a modest knowledge of the economic aspects. Despite the slightly higher percentage of physicians providing the correct answers on economic aspects, nurses’ average normalized score was almost the same as the physicians’ (3.6/10 vs. 3.4/10). Hypothesis H1 is only partially confirmed. Administrative staff and physicians feel more confident than nurses in providing estimates of economic factors; however, nurses demonstrate, on average, the same capability as physicians to evaluate DRG costs and rate. The survey also indicates that doctors and nurses, on average, are more aware of the costs of the activities in which they are directly involved than any other economic aspect.

H2 is confirmed: data show that the EFI is higher for the administrative staff, followed by physicians, and then by nurses. H3 is disconfirmed, as data suggest that the informative gap is unrelated to the length of work experience.

Nurses and physicians have limited awareness of the economic aspects of DRGs, yet they consider these aspects critical. In most cases, the estimates provided by medical and nursing staff on the costs of the resources used in the process were far from reasonable. Among the nurses, more than half (i.e., 19) scored 0 or very close to 0, but only five respondents did not regard economic aspects as significant. 15 of the 22 physicians scored less than 5/10, while only one considered the financial aspect not important. This indicates an informational gap that needs to be addressed.

4.2Addressing the information gaps

Findings show that different professional groups have different EFA and attach different levels of importance to the economic aspect. This suggests that the information gap may manifest differently across different professional groups, with different groups needing different types of information. Providing extensive economic and financial data indiscriminately to all staff may not be beneficial. The administrative department has to monitor the hospital’s ability to cover costs; for this reason, they must recognize any waste of resources and evaluate the margin generated by each DRG to cover overheads. Thus, the administrative staff is particularly interested in assessing DRGs’ margins to cover common costs. The analysis indicates that this margin is negligible on DRG 546. Consistent with findings from other studies,[3, 5] the operating room cost affects the overall DRG cost more significantly than other clinical care areas. Some expenses depend on time spent on activities or the number of inpatient days, while others are patient-specific (e.g. prostheses). Since patient-specific factors influence costs, the DRG margin varies based on each patient’s condition.

DRGs’ rates are fixed but offset by costs that vary depending on multiple factors, some of which are controllable by the hospital (e.g., the number of days of hospitalization), while others are not (e.g., prostheses). Fixed DRG rates aim to hold hospitals accountable for their efficiency by encouraging cost containment. However, a fixed rate also transfers the risk associated with patient-specific costs to the hospital. To mitigate this, reimbursement for patient-specific expenses should be extrapolated from the rate to cover only costs depending on the hospital’s efficiency level.

Regarding medical and nursing staff, reducing the information gap requires understanding its causes and the specific information needs of each category. Both doctors and nurses have demonstrated a certain level of economic awareness (EFA) for activities requiring their direct involvement and for medical devices, while they are largely unaware of other economic aspects, including the DRG rate.

The lack of EFA can be attributed to two main factors. Firstly, medical and nursing staff pay more attention to care issues than managerial aspects: their time is almost entirely dedicated to patient care and treatment, with increasingly heavy workloads due to the structural shortage of healthcare personnel throughout the Italian healthcare system. Physicians often consider patient care as their sole responsibility. However, the study’s findings, particularly the data on the importance of EFI, suggest that this does not preclude physicians’ interest in economic aspects. This awareness enables them to make informed decisions that, while prioritizing the patient’s primary interest, respecting medical autonomy, and adhering to medical protocols, also safeguard the hospital’s economic sustainability.

Secondly, administrative staff do not convey economic information to other professional groups because they do not know exactly what information is needed. Financial information is not communicated to healthcare personnel even when it is readily available (such as the DRG rate), and conveying it would not require any sophisticated control system. It is therefore necessary to (a) understand what information might be useful for doctors and nursing staff and then (b) define how it should be collected and reported to the recipients.

If, on the one hand, administrative staff do not know doctors’ and nurses’ information needs, on the other hand, healthcare staff lack financial skills and do not know exactly what information they could request. Training medical and nursing staff would thus be a first step towards reducing the information gap. However, providing them with too much financial information could be as counterproductive as not providing any at all. Based on cost accounting principles, it can be stated that the information useful to doctors and nurses pertains exclusively to the so-called relevant costs, i.e., costs associated with alternative methods of executing a specific phase of the therapeutic process while maintaining an unchanged level of appropriateness. All costs that do not show variations between alternative treatment methods are not modifiable and, therefore, are not interesting to clinical staff. In other words, it is not important for clinical staff to know “the cost of the DRG” or “all the costs of the resources used” but only the cost of those resources used differently in alternative clinical treatments resulting in the expected patient outcome. This implies that the information gap of clinical staff should be filled by starting to identify the resources whose use changes in relation to possible alternative treatments.

Another consideration must be made regarding the cost of activities performed (such as clinical exams and other procedures conducted during the patient’s stay or operation). It is essential to compare activity costs with the potential benefits for the patient. Identifying activities that incur costs without providing significant patient benefits or only yielding negligible effects is crucial. Such activities should be eliminated. This evaluation should be conducted by the physician, considering both the cost and the clinical value of the activity. Therefore, the hospital should maintain a list of activities that do not impact the appropriateness of the therapeutic process if omitted.

Certain professional roles are pivotal in identifying and reporting relevant information. For instance, nursing coordinators involved in procurement and inventory management have access to economic data and can assist administrative staff in identifying pertinent information based on the principles outlined.

4.3Limitations and future directions

The primary limitation of this study is its focus on a single hospital. Additionally, the hospital is part of a public healthcare system financed through DRGs, where the reference context can significantly influence the availability of cost information and cost awareness among hospital staff. Furthermore, only one DRG is considered. While this aspect has little impact on measuring the importance attributed to economic aspects — since the relevant questionnaire question was general and did not specifically refer to DRG 546 — all questions on cost awareness specifically referred to this DRG. Therefore, awareness of the economic aspects of other DRGs could differ. Given that the study is based on the analysis of a single case, the results are not generalizable. However, the aim was not to provide definitive data on the information gap but to assess whether this gap can manifest differently across various professionals and phases of patient treatment.

Another limitation of the analysis is the lack of investigation into what information on economic aspects medical staff and nurses believe they need in the specific context of DRG 546. This should be the starting point for each hospital to define the contents of the economic information system to support doctors and nurses effectively and may be a future direction of research.

Authors contributions

The research design and the final version of the paper are attributable to Guido Modugno. DRG costing and the administration of the questionnaire were performed by Mario Casolino. Both coauthors developed the methodology and the literature review. Tina Corelli, Martina Vardabasso, and Alessandra Rachelli contributed to the data collection and analysis.

Ethical statement

The present study conformed to the principles outlined in the Declaration of Helsinki and was performed with the approval of the Ethics Committee of Institute for Maternal and Child Health - IRCCS “Burlo Garofolo” (No. 31/23). Written informed consent was received from all study participants.

Funding

This work was supported by the Italian Ministry of Health through the contribution given to the Institute for Maternal and Child Health IRCCS Burlo Garofolo, Trieste - Italy.

Conflicts of Interest Disclosure

The author declares that there is no conflicts of interest.

Ethics approval

The Publication Ethics Committee of the Sciedu Press. The journal’s policies adhere to the Core Practices established by the Committee on Publication Ethics (COPE).

Provenance and peer review

Not commissioned; externally double-blind peer reviewed.

Data availability statement

The data that support the findings of this study are available on request from the corresponding author. The data are not publicly available due to privacy or ethical restrictions.

Data sharing statement

No additional data are available.

Acknowledgements

The authors would like to thank the anonymous reviewers for their suggestions that made it possible to improve the article by making it clearer or readers unfamiliar with Italian healthcare.

References

- Chapman C, Kern A, Laguecir A. Managing quality of cost information in clinical costing: evidence across seven countries. Journal of Public Budgeting, Accounting & Financial Management. 2022;34(2):310-329. doi:10.1108/JPBAFM-09-2020-0155

- Kaplan R, Porter M. How to solve the cost crisis in health care. Harvard Business Review. 2011;89(9):46-52. https://www.vbhc.nl/wp-content/uploads/2021/10/Robert-S.-Kaplan-Michael-E.-Porter-How-to-Solve-The-Cost-Crisis-In-Health-Care-Harvard-Business-Review-2011.pdf

- Sirizi M, Barouni M, Mahani A. Analysis of cost price and net profit of paraclinic services in private and public sectors: a case study of Kerman city 2014. Health Management & Information Science. 2015;2(4):138-143. https://jhmi.sums.ac.ir/article_42655_439218389a585133843db52443d101b4.pdf

- Tan S, Rutten F, Van Ineveld B. Comparing methodologies for the cost estimation of hospital services. The European Journal of Health Economics. 2009;10:39-45. doi:10.1007/s10198-008-0101-x

- Chandawarkar R, Taylor S, Abrams P. Cost-aware care: critical core competency. Archives of Surgery. 2007;142(3):222-226. doi:10.1001/archsurg.142.3.222

- Guidet B, Beale R. Should cost considerations be included in medical decisions? Yes. Intensive Care Medicine. 2015;41:1838-1840. doi:10.1007/s00134-015-3988-6

- Nouroozi T, Salehi A. Prime costs of clinical laboratory services in Tehran Valiasr Hospital in 2009. Eastern Mediterranean Health Journal. 2013;19 :s159-65.

- Levine D, Cole B, Rodeo S. Cost awareness and cost containment at the Hospital for Special Surgery: strategies and total hip replacement cost centers. Clinical Orthopaedics and Related Research. 1995;311:117-124. http://www.pacificaortho.com/downloads/sek/ccandcc.pdf

- Linna M, Häkkinen U, Peltola M. Measuring cost efficiency in the Nordic Hospitals-a cross-sectional comparison of public hospitals in 2002. Health Care Management Science. 2010;13:346-357. doi:10.1007/s10729-010-9134-7

- Hrifach A, Brault C, Couray-Targe S. Mixed method versus full top-down microcosting for organ recovery cost assessment in a French hospital group. Health economics review. 2016;6:53. doi:10.1186/s13561-016-0133-3

- McGrath M, Feroze A, Nistal D. Impact of surgeon rhBMP-2 cost awareness on complication rates and health system costs for spinal arthrodesis. Neurosurgical Focus. 2021;50(6):E5. doi:10.3171/2021.3.FOCUS2152

- Ellwood S, Chambers N, Llewellyn S. Debate: Achieving the benefits of patient-level costing-open book or can’t look?. Public Money & Management. 2015;35(1):69-70. doi:10.1080/09540962.2015.986893

- Špacírová Z, Epstein D, García-Mochón L. A general framework for classifying costing methods for economic evaluation of health care. The European Journal of Health Economics. 2020;21(4):529-542. doi:10.1007/s10198-019-01157-9

- Ryan J, Rogers A, Robb W. A study evaluating cost awareness amongst surgeons in a health service under financial strain. International Journal of Surgery. 2018;56:184-187. doi:10.1016/j.ijsu.2018.06.027

- Drummond M, Sculpher M, Claxton K. Methods for the Economic Evaluation of Health Care Programmes (Third Edition). Oxford University Press. 2005. doi:10.1093/oso/9780198529446.001.0001

- Zepeda E, Nyaga G, Young G. On the relations between focus, experience, and hospital performance. Health Care Management Review. 2021;46(4):289-298. doi:10.1097/HMR.0000000000000283

- Tan S, Serdén L, Geissler A. DRGs and cost accounting: Which is driving which. Diagnosis-related groups in Europe: moving towards transparency, efficiency and quality in hospitals. Edited by Busse., R, Geissler, A, Quentin, W, Wily, M. Buckingham, Open University Press and WHO Regional Office for Europe (2011a). 2011: 59-74. https://www.researchgate.net/publication/284143972_DRGs_and_cost_accounting_Which_is_driving_which#fullTextFileContent

- Mulholland D, O’Neill D, Redmond C. Cost awareness of interventional radiology devices among radiology trainees. Irish Journal of Medical Science. 2021;114(1):236.

- Clement F, Ghali W, Donaldson C. The impact of using different costing methods on the results of an economic evaluation of cardiac care: microcosting vs gross-costing approaches. Health Economics. 2009;18(4):377-388. doi:10.1002/hec.1363

- Guerre P, Hayes N, Bertaux A. Estimation du coût hospitalier: approches par «micro-costing» et «gross-costing» [Hospital costs estimation by micro and gross-costing approaches]. Revue d’Épidémiologie et de Santé Publique. 2018;66:S65-S72. doi:10.1016/j.respe.2018.02.001

- Frick K. Microcosting quantity data collection methods. Medical Care. 2009;47:S76. doi:10.1097/MLR.0b013e31819bc064

- Chapman C, Kern A, Laguecir A. International Approaches to Clinical Costing. Healthcare Financial Management Association (HFMA). 2013. http://www.hfma.org.uk/costing/supporting-material/

- Chapko M, Liu C, Perkins M. Equivalence of two healthcare costing methods: bottom-up and top-down. Health Economics. 2009;18(10):1188-1201. doi:10.1002/hec.1422

- Potter S, Davies C, Davies G. The use of micro-costing in economic analyses of surgical interventions: a systematic review. Health Economics Review. 2020;10(1):3. doi:10.1186/s13561-020-0260-8

- Mogyorosy Z, Smith P. The main methodological issues in costing health care services: a literature review. Centre for Health Economics, University of York Working Papers, (007cherp). 2005. https://www.york.ac.uk/media/che/documents/papers/researchpapers/rp7_Methodological_issues_in_costing_health_care_services.pdf

- Keel G, Savage C, Rafiq M. Time-driven activity-based costing in health care: a systematic review of the literature. Health Policy. 2017;121(7):755-763. doi:10.1016/j.healthpol.2017.04.013

- Cooper R, Kaplan R. Measure costs right: make the right decisions. Harvard Business Review. 1988;66(5):96-103. https://hbr.org/1988/09/measure-costs-right-make-the-right-decisions

- Cannavacciuolo L, Illario M, Ippolito A. An activity-based costing approach for detecting inefficiencies of healthcare processes. Business Process Management Journal. 2015;21(1):55-79. doi:10.1108/BPMJ-11-2013-0144

- Phan Y, Hadjipavlou M, Abdalla O. Cost awareness in urology: a nationwide survey. Journal of Clinical Urology. 2020;13(1):25-32. doi:10.1177/2051415819856791

- Schilling U. Cost awareness among Swedish physicians working at the emergency department. European Journal of Emergency Medicine. 2009;16(3):131-134. doi:10.1097/MEJ.0b013e32831cf605

- Hernu R, Cour M, de la Salle S. Cost awareness of physicians in intensive care units: a multicentric national study. Intensive Care Medicine. 2015;41:1402-1410. doi:10.1007/s00134-015-3859-1

- Fabes J, Avsar T, Spiro J. Information Asymmetry in Hospitals: Evidence of the Lack of Cost Awareness in Clinicians, Applied Health Economics and Health Policy. 2022;20:693-706. doi:10.1007/s40258-022-00736-x

This work is licensed under a

This work is licensed under a